This week I read a story in the National Post* about how many dollars ($532 million) are sitting in the Bank of Canada vaults waiting for their owners (1.4 million of them) to claim them. The money legally belongs to Canadians and it doesn’t require wiring any funds to Nigeria to get at it. Personally I hold onto my money as tightly as a limpet does an ocean rock at low tide so there is no chance any of those “lost accounts” belong to me. One once belonged to a close personal relative though! If one belongs to you, here’s how to get your old bank balance back from a forgotten account.

* For some reason we’re getting the Post for free this week. One of the advantages (?) of our neighbourhood is we often get newspapers for free as they try to hook us on them and get us to subscribe. The weirdest year was when we were getting the TorStar because the Blue Jays had sponsored it.

You may be wondering why the Bank of Canada now is the proud home of your $28.17.

Essentially, Canadian banks are regulated. To keep things honest, there are rules about how long an account can be left inactive. If an account at a regular bank branch (or credit union etc.) has been inactive for more than 10 years, the balance is transferred to the Bank of Canada. They hold onto balances of under $1000 for another 30 years. They hold onto balances of over $1000 for 100 years. If no one claims those balances within the holding period they are given to the Receiver General for Canada, a.k.a. the federal government who will promptly spend it on Senators’ expenses.

Who Could Possibly Forget They Had a Bank Account with Money In It?

Frankly, many of these accounts belong to people who have died. They may have had two or more bank accounts and their heirs only knew about one. Or they may not have had any heirs.

Other accounts belong to people who suffered from a mental illness and lost track of them.

Some, like my relative’s, got transferred to the Bank of Canada due to negligence. He always planned to visit the bank and get the money out but he procrastinated so long it ended up inactive.

I suspect, but I cannot prove, that some accounts are left open with tiny balances because the financial institution will charge a large fee to close the account. I’ve certainly heard anecdotally that this happens.

And, some, as this witty post by IPlom on RedFlagDeals pointed out, belong to people who have so much money they literally don’t care about the nickels and dimes:

The Bank of Canada is also holding onto other types of investments including

- GICs

- bank drafts

- term deposits

- positive credit card balances (!) and

- traveller’s cheques

While it’s hard to imagine anyone having a positive credit card balance, especially since now most CCs charge a $10 fee for any inactive cards with a balance, I can see where someone might have a $50 or $100 traveller’s cheque they misplaced and never cashed.

Where Do I Start to Get My Money Back from an Old Bank Account?

Everything will be easiest if you have your old bank book and you live within a reasonable distance of your old branch. In that case, you can re-claim the balance by visiting that branch and getting the paperwork filled in and submitted.

What if you don’t have a bank book or any statements and you’ve moved half a country away? Don’t worry there’s a process for that too.

Checking Which Old Bank Accounts the Bank of Canada is Holding

If you’re like me and always secretly wished you had a reclusive Great Great Uncle that you’d never met (and therefore would not honestly grieve the loss of) who would suddenly die leaving you the sole heir of hundreds of millions of dollars, you may want to search for more than your own old unclaimed bank accounts at the Bank of Canada.

You can search the Bank of Canada database for the names of any of your relatives. Only the person themselves or a legal heir can claim the money, of course, but if you were heir or part heir of an estate that might be you! Or your rich second cousin twice removed my give you a finder’s fee for reminding them about that paltry $200 000 account they forgot about in Chibougamau.

Besides it’s fun! (Ok, remember my alternative is supervising one of my children memorizing the Periodic Table of Elements. Valences of Tantalum anyone? Anyone at all?)

How to Check Whether the Bank of Canada Has Any Old Accounts Related to You

- Open your internet browser and go to the site: http://www.bankofcanada.ca/unclaimed-balances/

- Click on the link called Search our unclaimed database.

- In the Name: field, type a full or partial name.

- From the Province/territory: drop-down list, either leave the default of All or select the specific province or territory of interest.

- Click on the Search button.

There is a good explanation of how to enter names on this page.

For example, they explain you can enter: John AND Brown to get a list of all names containing only “John” and only “Brown” such as John Brown; John E Brown; James John Brown Smith; etc.

It also warns the website may crash on the weekends or after hours. If it does, it will not be repaired until regular business hours from Monday to Friday 8 a.m. to 5 p.m. ET. I guess they figure if you’ve waited over 10 years to get your money back, you can wait another few days.

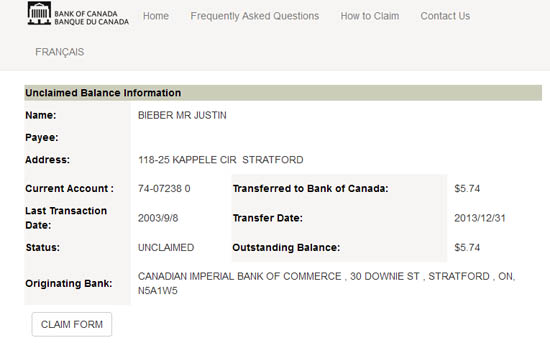

What Information Is Provided by the Bank of Canada About the Unclaimed Balance?

Obviously they are not going to play detective and try to find out lots of information about the money they receive. So their records are only as complete as those of the financial institution that sent them in.

An example record for Jane Smith lists

- the name and address of the bank that sent in the money

- the amount of money

- the date that the bank account was used last

- the date the money was sent to the bank of Canada (10 years later on December 31)

If you think that is your bank account, you click on the Claim Form button.

The Unclaimed Balance Information Payment Authorization Form will open.

(It is not valid for a claim by the Estate of a person who has died.)

Print it out.

How to Claim Your Unclaimed Balance from the Bank of Canada

To complete the form

In the Step 1 section of the form, you should fill in your

- Name

- Address

- Phone Number

Then you sign it and date it.

Next, you have to take or send the form, to the branch that held the account. You may want to bring or include copies of any information you have about the account such as your bank book or a statement

That bank has to compare your signature with the information they have on file for the account. If they agree that it matches. They will add their authorizing stamp, name, signature and date to Step 2 of the form.

Then you or they mail the completed form to the Unclaimed Balances Services address given on the form.

How Do I Claim the Unclaimed Balance for an Estate or In Special Circumstances?

There are good detailed explanations of how to make a claim

- for an Estate

- for an Organization that no longer exists

- if the bank branch has closed

- for non-bank assets such as a traveller’s cheque

on the Bank of Canada website at: http://www.bankofcanada.ca/unclaimed-balances/how-to-claim/

How Fast Will I Get My Money Back?

The Bank of Canada site says it will take 30-60 days to settle a routine claim. You’ve already waited for at least 10 years, so you should be used to waiting!

Does It Work?

It did for my relative. He sure was glad to get that $17.52 back. Would an Honest Crooks lie to you?

Related Reading

Join In

Did you or someone you know ever have to reclaim a balance from the Bank of Canada? Did they decide after looking at the paperwork to just donate the money to the government? Please share your experiences with a comment.